Anyone doubting the stock market rally has legs should just have a short conversation with Ken Fisher. The billionaire investor has kept a bullish stance for a while, swatting away any bearish arguments and keen to point out he has been proven correct in his outlook.

“My 2023 forecast foresaw a global bull market, inflation cooling, no deep global recession and technology and other growth stocks leading. So it was,” said Fisher, whose investing endeavors have netted him a personal fortune of ~8.5 billion.

Any concerns around the ongoing bull market, such as the dominance of the Magnificent 7 stocks or that we might be reaching bubble stages are also given short shrift. “We aren’t near euphoria – which all these ‘Magnificent 7’ doubts prove,” the Fisher Investments founder went on to add. “That ‘It’s Just’ skeptical, doubt-ish talk never flourishes in bubbles. Sure didn’t in 2000. It takes a long, long time for pessimism to warm into euphoria. We may be straddling somewhere between skepticism and optimism now.”

So, with the bull market set to continue, where does Fisher think investors should be parking their cash? We can look at some of the names nesting in his portfolio to get an idea about that.

With this in mind, we decided to take a closer look at two rather different heavyweight names – Advanced Micro Devices (NASDAQ:AMD) and Eli Lilly (NYSE:LLY) – for whom Fisher’s investments are currently worth billions and find out what makes them good investing ideas at present. With help from the TipRanks database, we can also see whether the Wall Street analysts are on the same page here.

AMD

AMD might not be part of the Magnificent 7 stocks, but it could be a likely candidate for inclusion, given the story unfolding. The semi-giant has been one of the market’s winners for a while now and was also one of last year’s star performers. That display has extended into 2024, with the stock up by 41% so far this year.

That said, AMD has not always been a favored name. Hark back to about a decade ago, and the struggling chipmaker was even facing the prospect of bankruptcy. Yet under the guidance of CEO Lisa Su, the company has risen from the ashes and over the past few years has steadily eaten away at Intel’s dominance in the CPU market. Now it is also seen as possibly the biggest challenger to Nvidia in the AI chip game.

While its earnings reports have not been quite as stellar as Nvidia’s, they have also been regularly solid. In the 4Q23 print, revenue climbed by 10.7% year-over-year to $6.2 billion, in turn outpacing consensus by $60 million. At the bottom-line, adj. EPS of $0.77 met Street expectations.

In a clear sign the company sees an opportunity in the fast-emerging AI chip market, it increased its 2024 Data Center GPU revenue forecast to ~$3.5 billion from $2 billion+ beforehand.

As for Fisher’s involvement, he remains long and strong. He counts 28,368,826 AMD shares in his portfolio, which currently command a market value of almost $5.75 billion.

The company also has a big fan in Rosenblatt’s Hans Mosesmann, who sees more good times ahead for the chipmaker.

“AMD’s execution has been flawless in the areas that matter for investors,” says the 5-star analyst. “DC CPU, client CPU, and new AI acceleration roadmap that we see capturing double-digit share by 2025. As the AI dynamic moves more and more to the ‘edge’, AMD’s existing presence in the market, the range of CPU/GPU/DPU/FPGA products, and disruptive ‘chiplet’ expertise are set to make AMD a true secular idea.”

Mosesmann, who ranks at 6th spot amongst the thousands of Wall Street stock experts given the accuracy of his predictions, has a Buy rating on AMD shares, along with a $250 price target, suggesting shares will post gains of ~21% a year from now. (To watch Mosesmann’s track record, click here)

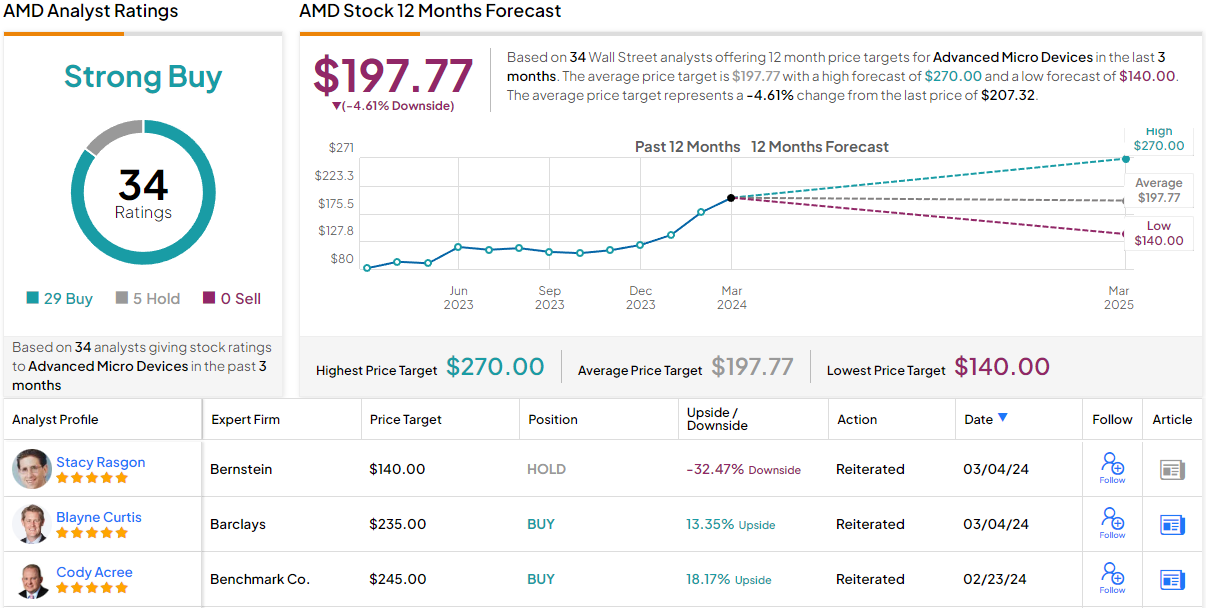

Most on the Street agree. Based on a mix of 29 Buys and 5 Holds, the stock claims a Strong Buy consensus rating. However, many seem to think the shares might need a breather. At $197.77, the average target implies the stock will drop ~5% from current levels. It will be interesting to see whether the analysts upgrade price targets over the coming months. (See AMD stock forecast)

Eli Lilly

If we’re on the subject of candidates for inclusion in the Magnificent 7 club, then one unlikely name could be up for consideration. Gatecrashing 2023’s AI-themed tech rally, Eli Lilly has been on an absolute tear, rising by 150% over the past 12 months. The stock now has a market cap of more than $754 billion, raising the prospect it could be the first pharma stock to cross the $1 trillion threshold.

The excitement around the pharma giant is down to its involvement in the weight-loss drug space and the development of a relatively new group of medicines called GLP-1 agonists, medications that can assist in the management of type 2 diabetes and obesity.

In November, LLY received FDA approval for its Zepbound (tirzepatide) injection, an innovative remedy for obesity. Zepbound works by stimulating both GIP (glucose-dependent insulinotropic polypeptide) and GLP-1 (glucagon-like peptide-1) hormone receptors. Tirzepatide is already on the market in the form of Mounjaro, a treatment for type 2 diabetes.

Both drugs helped LLY deliver a strong set of results in Q4. Mounjaro reached sales of $2.2 billion, outpacing consensus at $1.8 billion. While only recently launched, Zepbound generated $175.8 million, ahead of the Street’s forecast of $140.7 million. These made up for a drop in the sales of blockbuster diabetes drug Trulicity, which saw a 14% year-over-year decline to $1.7 billion.

All told, the company generated revenue of $9.35 billion, representing a 28.1% improvement on the same period a year ago and outpacing analyst expectations by $380 million. On the bottom line, adj. EPS hit $2.49, beating the Street’s call by $0.12. For 2024, revenue is anticipated to be in the range between $40.4–41.6 billion. Consensus was looking for $39.1 billion.

Meanwhile, Fisher obviously retains confidence in the story unfolding. He is holding a big LLY bag of 4,544,585 shares. At the current share price, these are worth more than $3.55 billion.

The company is not resting on its laurels and amongst other drugs is also developing a weight loss pill called orforglipron, which so far has shown promise in its clinical testing. Morgan Stanley’s Terence Flynn thinks the drug could be crucial to LLY in the years ahead.

“We believe the key question for the stock is whether expectations for LLY’s ~$70- 80bn in revenues in early 2030’s will continue to go higher,” Flynn said. “To answer this question, we are most focused on the dynamics within the US market (i.e., the ~$65bn revenue expectation), as it represents the majority of the commercial opportunity and we believe it will be viewed as a proxy for other geographies.”

“Bottom line is we believe the risk/reward in LLY is still skewed to the upside based on continued de-risking of Orforglipron (as patient exposure continues to build and enrollment in the Ph3 trials completes later this year into next year), relative to the risk of failure of the program due to a safety issue – hence no news is good news in our opinion,” the analyst went on to add.

To this end, Flynn has an Overweight (i.e., Buy) rating on LLY shares, backed by a $950 price target. The implication for investors? Upside of 21% from current levels. (To watch Flynn’s track record, click here)

Of the 19 LLY reviews posted during the past 3 months, 16 Buys outgun 3 Holds, making the consensus view here a Strong Buy. That said, given the constant gains, the $816.35 average target now makes room for only modest returns of 3% over the one-year timeframe. (See Eli Lilly stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.