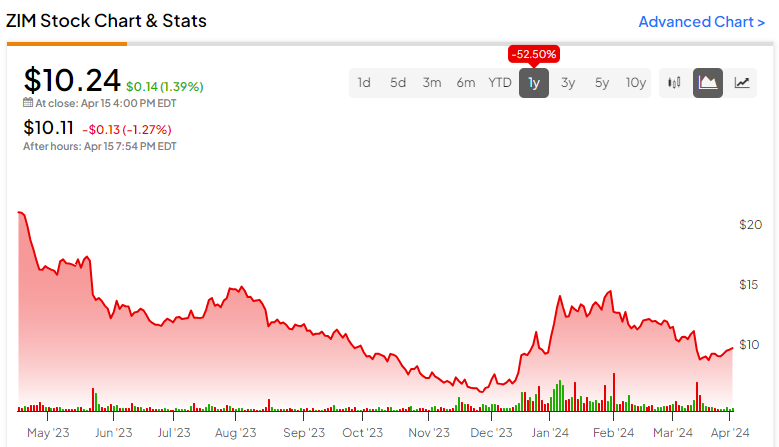

ZIM Integrated Shipping Services (NYSE:ZIM) stock has been volatile and is down 52.5% over the past 12 months (see below). The Israeli company has had to endure some challenging macroeconomic conditions as it goes through its own transition phase. However, I’m bullish on ZIM, with the firm reorienting itself towards becoming one of the most cost-efficient cargo shipping companies in the long run. I also acknowledge several near-term tailwinds.

The Volatility of the Shipping Sector

The shipping industry is currently experiencing something of a hangover. In 2021 and early 2022, the sector boomed on the back of strong demand for consumer goods and a resurgent global economy following the pandemic. ZIM and its peers performed well. In fact, ZIM stock traded nearly as high as $90 per share before it came crashing down.

However, more recently, concerns about a global recession and rising interest rates have resulted in demand for shipping services moving in the opposite direction. On top of that, shipping companies are still grappling with high fuel costs, partially resulting from Russia’s war in Ukraine and other rising operational expenses. The future is uncertain.

After a period of strong growth, the shipping industry is in a state of adjustment. Companies are increasingly looking to make strategic adjustments by investing in more efficient ships and exploring new technologies.

ZIM’s Fleet Upgrade: The Pros and Cons

ZIM is one of the oldest shipping lines in operation, but it’s investing in a transition program — with 46 newbuild vessels coming online — in order to sure up its future. Some 28 of these vessels will be LNG powered, and 24 of the 46 had been delivered as of 13 March. The remaining 22 are to be delivered in 2024. The goal is to replace its older, less fuel-efficient fleet with a modern one built for cost savings and environmental responsibility.

“Our core fleet will be modern, larger, and better suited to the trades in which we operate,” the company said in its Q4 update.

It’s also worth noting that ZIM’s business model is quite different from its competitors due to its heavy reliance on chartering vessels instead of owning them. This reduces CapEx but does make it more vulnerable to fluctuations in charter rates.

However, the aforementioned transition program, coupled with falling demand for ZIM’s services, has seen the company’s debt position increase. The newbuild program was initiated in 2021 and 2022, and the lease liabilities on the company’s balance sheet are expected to continue rising until the delivery of the last vessel. At the end of 2023, the company’s net debt position hit $2.3 billion, compared to net cash of $279 million as of December 31, 2022.

ZIM’s Revenue Tailwinds

So, it’s clear that ZIM is transitioning during a challenging period for the industry, and this is bound to put more strain on the company. However, there are some near-term tailwinds, which management expects to positively impact revenue generation. These tailwinds are Houthi attacks on vessels transiting the Red Sea in the context of broader regional tensions and the drought impacting transit through the Panama Canal.

Like many other companies, ZIM has made the decision to divert all vessels that were originally destined to pass through the Red Sea around the Cape of Good Hope until further notice. ZIM’s management estimates that longer voyages around the Cape have absorbed approximately 6% to 7% of global capacity. Coupled with vessels queuing and re-diverting because of the Panama drought, the availability of global supply has been falling, thus pushing up prices.

“While this disruption had minimal impact on our Q4 results, we expect first-quarter and potentially second-quarter earnings in ’24 to reflect the improved spot rates,” management stated.

Management’s guidance is somewhat vague, but it reflects the uncertainties concerning the above tailwinds. The company has guided for adjusted EBIT to be between -$300 million and $300 million. While I agree that leasing rates will decline rapidly once the Red Sea becomes navigable again, the current assumptions are very conservative.

Currently, there appears to be very little sign that Houthi activity will significantly decline. In fact, Iran’s seizure of the MSC Aires and subsequent direct attack on Israel could result in a further escalation.

In short, ZIM’s near-term performance hinges heavily on geopolitical events and, perhaps to a lesser extent, the weather. Given the trajectory of geopolitical events and tensions in the Middle East, I’m expecting ZIM to deliver an upside surprise in H1 at least.

Is ZIM Stock a Buy, According to Analysts?

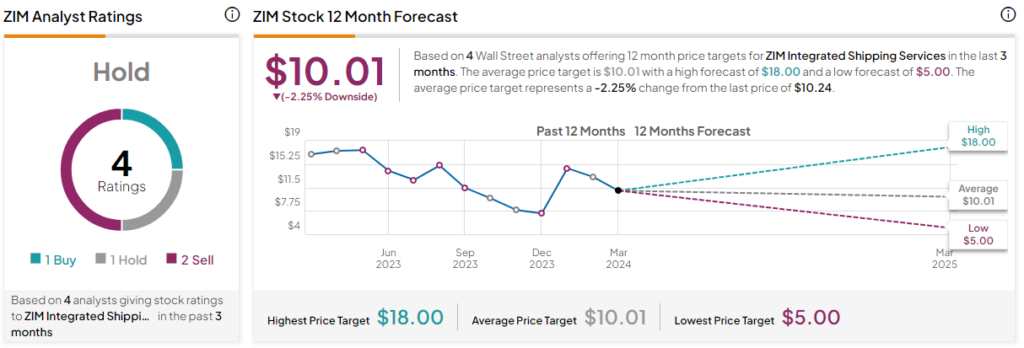

ZIM stock currently has a Hold rating based on one Buy rating, one Hold, and two Sell ratings given by analysts in the past three months. The average ZIM Integrated Shipping Services stock price target is $10.01, with a high forecast of $18.00 and a low forecast of $5.00. The average price target represents a -2.25% change from the last price.

The Bottom Line on ZIM Stock

ZIM’s stock price has fallen due to a rough patch in the shipping industry. Demand for shipping has dropped as the global economy is struggling, and fuel costs remain high. However, ZIM is investing in a major fleet upgrade with more fuel-efficient and environmentally friendly LNG-powered ships. This should make it a leader in cost-effective cargo shipping in the long run, albeit negatively impacting the company’s debt position in the near term.

In the short term, disruptions in the Red Sea and Panama Canal are reducing shipping supply and pushing up prices, which could benefit ZIM. While there’s uncertainty about how long these disruptions will last, ZIM might outperform expectations due to these factors.